Mapping the Operating Systems of Australian Christian Higher Education

Series: The Future of Formation (Part 1 of 4)

By Geoff Folland

April 2026

I took my first Bible college class in 1992, during my first year working as an auditor with a Big 4 firm. I wanted to broaden my understanding of evangelism beyond the practical lessons I had learned through Power to Change, so I enrolled in an evening class at what was then known as Emmaus Bible College.

I chose the college because I knew the faculty, it was down the road from my church, and my grandfather had been on the founding board.

Three years later, when I joined Power to Change as a missionary, I signed up for the SMBC Preaching Conference. Dick Lucas. James Montgomery Boice. John Chapman. That experience reshaped how I thought about preaching and ministry.

Later, when I decided to pursue an MDiv, I studied part-time at Morling College. I chose Morling because it was across the creek from my ministry at Macquarie University.

Over time, I’ve hosted student missions from SMBC, supervised interns from Morling, been a guest lecturer at other colleges, graded papers for ACOM, and attended events across the country.

From the inside, it feels like a diverse ecosystem. From the outside, it looks fragmented.

Both are wrong.

Ask a Sydney Anglican to describe a Bible college, and they will point to a residential campus in Newtown with a serious academic library and a strong sense of community. Ask a Pentecostal leader, and they will describe a national network of hubs embedded in local churches. Ask a Melbourne academic, and they will describe a collegiate university deeply integrated into the higher education research sector.

All three are correct. Yet they are describing entirely different systems.

The Sector Architecture and the “Operating Systems”

The Australian theological education sector collectively holds well over $350 million in assets, yet it remains largely invisible even to many of the leaders who rely on it. Most denominational executives, board members, and donors operate within a field of vision shaped by their own experience, unaware of the architecture beyond it.

To understand where Christian formation is going and why solvency pressure is increasing, we need to see that architecture clearly.

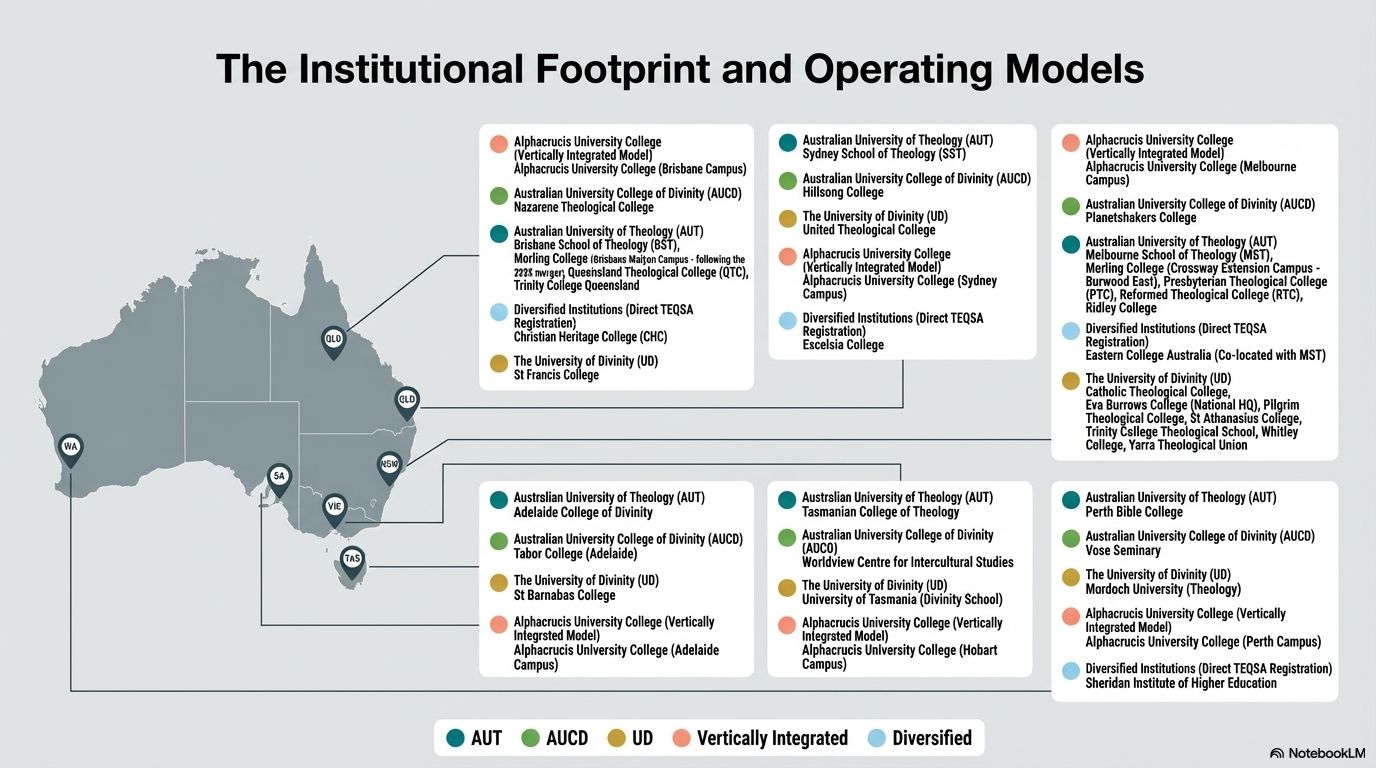

There are not fifty independent colleges scattered across the country. Much of the sector is organised around a small number of underlying systems, with a growing group of independent providers pursuing different strategies alongside them.

The first three operate as shared accreditation systems.

The University of Divinity

In Melbourne, the University of Divinity functions as a collegiate university. Distinct colleges—Catholic, Anglican, Uniting, Salvation Army, Baptist—participate in a shared academic and governance structure. It is research-led, academically rigorous, and ecumenically integrated.

The Australian University of Theology (AUT)

Across the evangelical sector, the Australian University of Theology operates as a distributed consortium. The university provides accreditation, curriculum, and compliance. Colleges such as SMBC, Ridley and Morling provide the teaching, community, and culture. It is standardised enough to scale, but flexible enough to preserve institutional identity.

Australian University College of Divinity (AUCD)

Alongside it sits the Australian University College of Divinity. Less visible, but strategically significant. Where the Australian University of Theology leans toward scale, AUCD leans toward flexibility. It enables smaller colleges, specialist providers, and diverse denominational communities to operate within the higher education framework without carrying the full regulatory burden themselves.

What follows are not shared systems, but institutional responses to them.

Alphacrucis University College

Alphacrucis University College represents a vertically integrated model. It owns its accreditation, its delivery, and its expansion strategy. It has built a national platform through campuses, partnerships, and church-based hubs.

Moore Theological College

Moore Theological College represents something different again. It does not sit on any shared system. It is self-accrediting, asset-backed, and deeply aligned to a single ecclesial vision. Where others share infrastructure, Moore carries its own. Where others distribute, Moore concentrates. It is a coherent model. It also depends on the level of capital held by a few institutions.

Another model is emerging alongside these.

Not built on shared infrastructure. Not driven by scale. Not sustained by legacy assets.

But by adaptation.

Diversified Institutions

Across the country, a growing number of colleges that began as Bible colleges have repositioned themselves as broader providers of Christian higher education. Institutions such as Tabor, Eastern, and Christian Heritage now offer degrees in education, counselling, business, and community services alongside theology. In many cases, these adjacent disciplines have become the economic centre.

The pattern is consistent. High-demand, government-supported programs generate the revenue. Theology becomes one stream among many—often smaller, sometimes shrinking, but still symbolically central.

This is not a new system. It is an institutional adaptation.

Where the traditional model depended on a pipeline of full-time ordinands, this model depends on diversified enrolments and FEE-HELP-supported degrees. Where once the institution existed to train ministers, it now exists to deliver a portfolio of outcomes—professional, academic, and formational.

It is a viable strategy. It also reframes the institution’s purpose.

For boards and denominational leaders, this is no longer a theoretical question. It is a governance decision about what kind of institution they are stewarding.

Once you see these systems, the landscape changes. What appears fragmented is, in fact, structured. What feels diverse is, in reality, patterned.

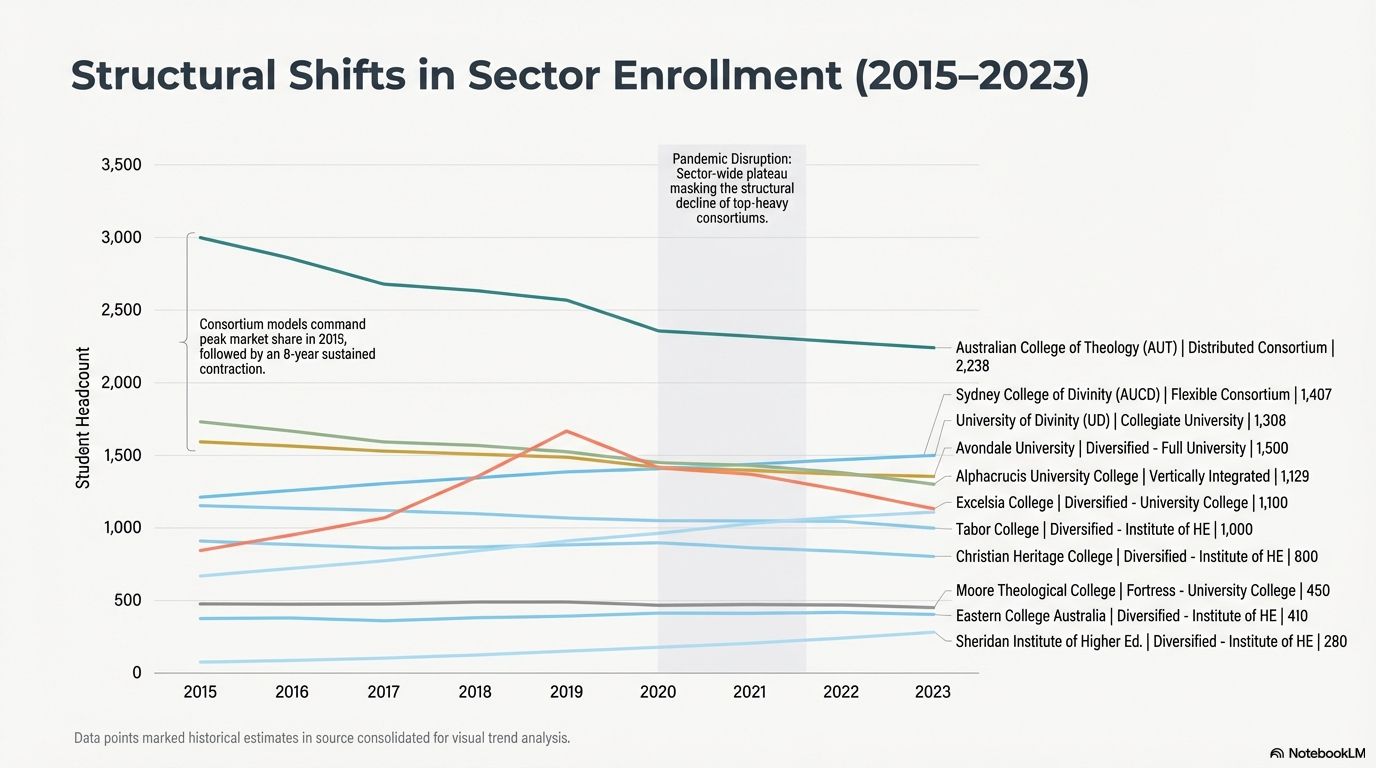

The tension we are now experiencing in the sector is not the result of failure. It is the result of timing.

Around the turn of the millennium, the vocational pipeline still held. Denominations produced young ordinands. Colleges trained them in residential communities. Churches employed them. Much of our current infrastructure—dormitories, dining halls, lecture theatres, and libraries—was built or expanded to serve that reality.

The Regulatory Pivot and the “Compliance Cost-Lock”

Then came the introduction of TEQSA (Tertiary Education Quality & Standards Agency) in 2012. The shift from “Bible college” to “higher education” lifted standards and strengthened governance. It also locked in a high fixed-cost model. Compliance became a permanent overhead, just as the underlying demand began to shift.

That change is now unmistakable.

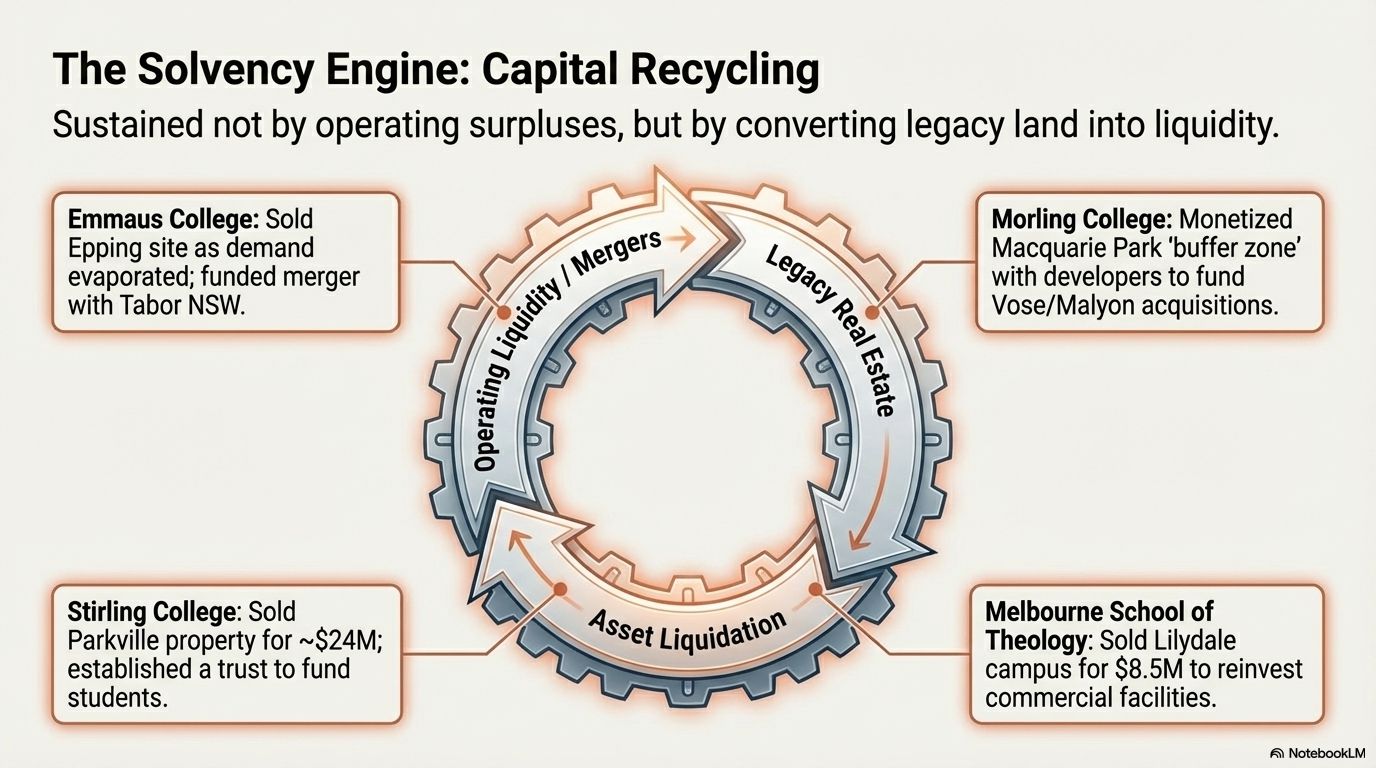

The Solvency Strategy and the “Capital Recycling” Reality

I first noticed it not in a report, but in a property sale.

Emmaus Bible College sold its site on Ray Road in Epping. For decades, it had been a training base for enthusiastic young Christian Brethren. But by the time of the sale, the student pipeline had already dried up. There were fewer young people in the denomination, and the emerging leaders I knew were no longer choosing Emmaus. They were choosing Morling, SMBC, or Moore.

The land was sold. The college relocated. Then merged. Then restructured again.

The asset was real. The demand was not.

Around the same time, the Churches of Christ College in Carlingford, NSW, was also sold. That decision proved more strategic. The proceeds were used to fund a merger with Kenmore Christian College (QLD), which became the Australian College of Ministries—an early move toward a distributed, asset-light model that no longer depended on residential infrastructure. Stirling College in Melbourne sold its Mulgrave property for approximately $18 million, but did not transfer the proceeds to ACOM. Instead, it set up a trust to fund students at ACOM.

Whitley sold its Parkville property for ~$24m. And Reformed Theological College relocated its teaching to Melbourne in 2017 and later sold its Geelong (Waurn Ponds) campus as part of a staged consolidation in Melbourne.

Then came a different signal altogether.

Morling began developing its Macquarie Park site in partnership with commercial developers, unlocking the value of prime real estate to fund expansion. Moore College, by contrast, doubled down—constructing a multi-storey academic and residential facility in Newtown, funded largely through its donor base. Even SMBC began expanding student accommodation.

Three colleges. Three responses to the same pressure: sell, pivot, or build.

These are not isolated stories. Across the sector, institutions have been selling, redeveloping, or repositioning assets in response to declining full-time enrolments and rising compliance costs. Funds from Emmaus’ Epping site were used to finance a merger with

Tabor NSW. Morling’s Macquarie Park development introduced high-density residential and commercial infrastructure into what was once purely educational land, funding the absorption of Vose (WA), and Malyon (QLD) and expansion to a Burwood East location in Melbourne.

Reformed Theological College relocated its teaching to Melbourne in 2017 and later sold its Geelong (Waurn Ponds) campus as part of a staged consolidation in Melbourne. Melbourne School of Theology sold its Lilydale campus for $8.5 million and reinvested in a commercial facility in Wantirna, which is now listed for sale.

This is not anecdotal.

It is systemic.

Australian theological education is increasingly sustained not by stable operating surpluses, but by capital recycling—converting land into liquidity to fund ongoing operations.

The “Customer” Shift: From Gary to Susan

At the same time, the student profile has fundamentally changed. The system was built for one kind of student, but it is now sustained by another. In 1995, the typical student was a 22-year-old ordinand. Let’s call him Gary. Gary studied full-time, lived residentially on campus, and was fully funded by his denomination. For the colleges, the economics of Gary were simple: high fixed costs (dormitories and dining halls), but predictable, full-time revenue over three to four years.

In 2026, the typical student is in her forties. Let’s call her Susan. Susan studies part-time while balancing a secular career or family. She engages online or through block intensives, and she is often self-funding her study via FEE-HELP. Her goals are broader—chaplaincy, non-profit leadership, or theological formation for the workplace. The economics have shifted with her: lower full-time equivalent (FTE) loads, fragmented per-subject revenue, and a demand for digital rather than physical infrastructure.

We built a physical infrastructure for Gary, but our revenue now relies on Susan.

The Institutional Response and the “Shadow Sector”

What happened to the Garys? The young leaders have not totally disappeared, but they are increasingly being trained outside the traditional degree system. They are opting for alternative pathways that bypass the formal academic structures entirely.

In some contexts, these pathways are no longer marginal. Large churches—such as the Planetshakers movement in Melbourne—are now training cohorts of ministry leaders internally at a scale that rivals, and often exceeds, historic colleges. Alongside them sits the parachurch pipeline. Organisations like Youth With A Mission (YWAM), Youth Dimension, and Power to Change are intercepting the post-school demographic by offering immersive campus internships and cross-cultural mission experiences. These pathways deliver high-impact formation without the high fixed-cost base, the FEE-HELP debt, or the compliance burden of the higher education sector.

Recognising this massive flight, the institutional sector has attempted to recapture the youth market by rapidly expanding its own one-year “Gap Year” diplomas and discipleship programs. Examples from Sydney alone include:

- Year 13 (Youthworks)

- The Bridge (SMBC)

- IMPACT (The Baptist / Morling College program, formerly known as Plunge)

While these, and others offered around Australia, are excellent formation programs, their very existence highlights the broader strategic reality: the traditional four-year residential seminary degree is no longer the default pathway for the next generation of leaders. The sector is having to innovate at the entry-level simply to maintain a connection with the young adults it was originally built to train.

The Infrastructure Duplication and the “Misaligned Map”

Geoff Folland

National Director

Power to Change