I’ve reviewed the published financial statements for each institution for the past five years. I don’t have the same understanding as I would in a Board meeting or with the executive teams. I have tried to represent each institution fairly. If you are not inside this system, the detail can feel complex. The principle is simple: some institutions have time. Others depend on flow.

In practice, this shows up in very ordinary ways. A college can feel busy—full classrooms, active community—and still struggle to cover its fixed costs, while another carries a deficit for years without immediate pressure. The difference is not activity. It is structure.

Why the numbers behave this way

At a basic level, the economics of a theological college are not complicated—but they are stubborn.

A significant portion of the cost base is fixed.

Buildings require maintenance whether they are full or half empty. Overall compliance costs under TEQSA do not scale down when enrolments fall. Core staffing, particularly faculty, sits in a middle category: not entirely fixed, but difficult to adjust without compromising the integrity of the offering. Once you appoint a lecturer in New Testament or Systematic Theology, that cost remains, even if student numbers fluctuate.

There are variable elements – adjunct teaching, casual staff, and some delivery costs – but they are not large enough to offset the fixed base.

Which means the system behaves predictably.

When student numbers grow, the model works. When they flatten, margins tighten. When they decline, deficits emerge quickly—and are difficult to reverse without structural change.

This is why the balance sheet matters.

It is what absorbs the gap between a largely fixed cost base and a volatile revenue stream.

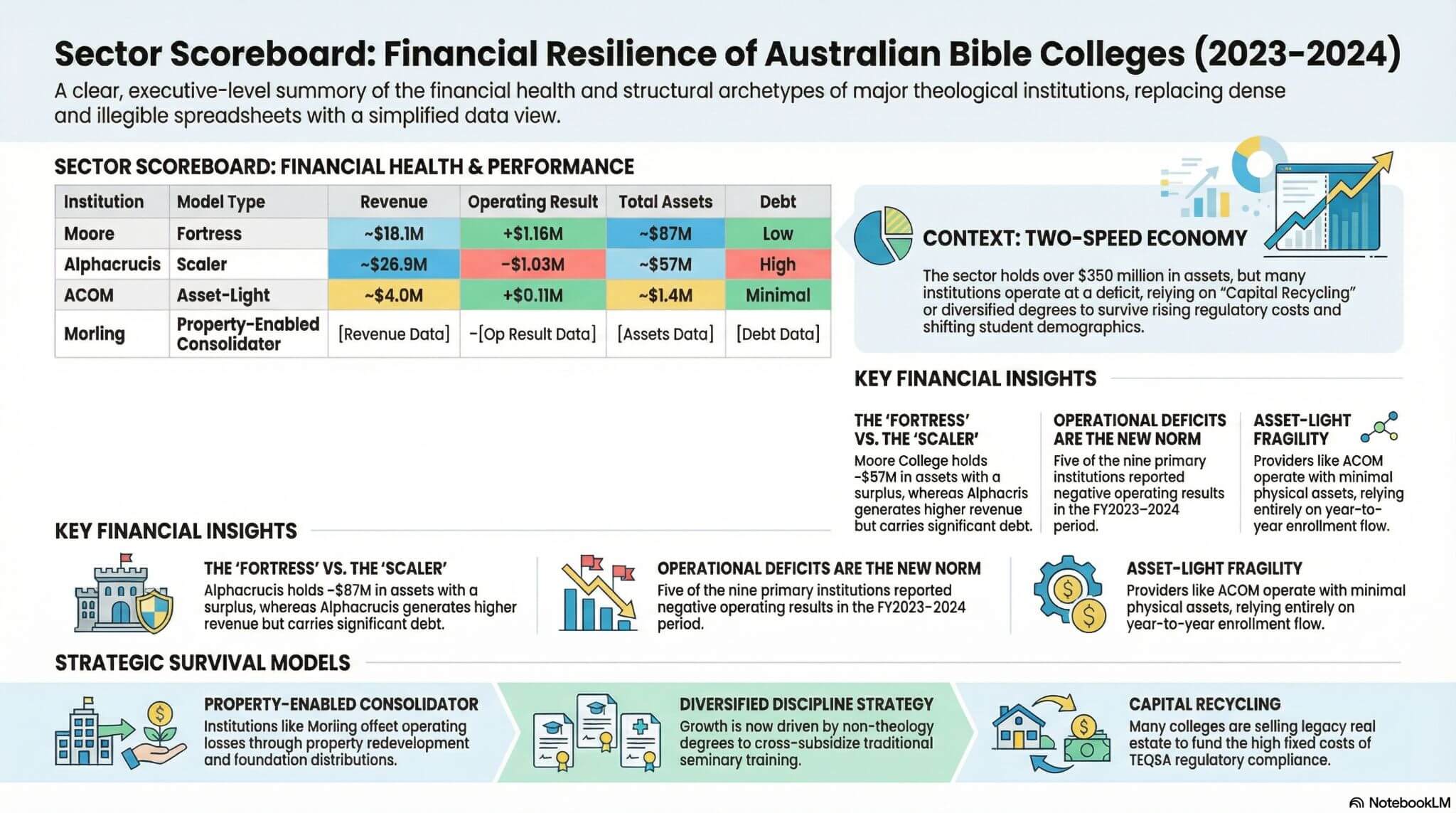

2. The Self-Accrediting Fortress

Moore remains the clearest example of a balance sheet buying time.

A large asset base creates options: deficits can be absorbed, decisions can be paced, and leadership can act deliberately. The fortress is not defined by comfort, but by time—the capacity to absorb pressure without being forced into immediate structural change.

That time, however, is not unlimited. Even strong institutions still face tightening margins, rising costs, and ongoing dependence on multiple income streams. A large balance sheet does not remove pressure; it simply extends the horizon until someone must address it.

A necessary contrast

Alphacrucis operates at scale and carries a significant asset base, but with a different risk profile. Borrowings are higher, growth assumptions are more embedded, and the system is more sensitive to shifts in enrolment or cost structures.

The distinction matters.

Structure, not status, determines resilience.

3. The Property-Enabled Consolidator

Morling represents a different response again.

Not eliminating deficits, but building a system around them.

Operating losses must be offset through foundation distributions, investment income, and property redevelopment. This is not accidental; it reflects deliberate strategic thinking about how to fund the present by reconfiguring the balance sheet, rather than expecting the operating model to carry the full load.

Across the sector, I have been struck by the number of thoughtful, creative responses leaders have developed.

A strong asset base at Moore. Property development at Morling. Foundation-linked models emerging through Stirling and ACOM. These are not naive strategies. They are the work of capable people responding to real constraints.

But they also reveal the tension beneath the system.

Scale consumes cash. And not every strategy resolves the pressure it is designed to address.

4. The Asset-Light Distributed Network

At the other end of the spectrum sits ACOM.

It operates with minimal assets and limited reserves, relying on current-year income to sustain delivery. Its strength is flexibility; its weakness is exposure, because the same structure that enables scale also removes any meaningful buffer when conditions tighten.

Removing buildings does not remove fragility—it simply changes its form.

The model can work, particularly at scale, but it depends on stable enrolments, stable funding settings, and stable partnerships.

The Stirling shift

The relationship between Stirling and ACOM makes the shift visible.

Stirling has stepped back from direct delivery and redirected its resources into a broader platform. Capital and delivery have been separated—held in different places, then partially reconnected.

This shift is not theoretical. It is already reshaping the system.

5. The Embedded College

United Theological College at North Parramatta illustrates something different again.

UTC operates as a theology campus in partnership with Charles Sturt University, but it should not be understood as a standalone financial entity. Instead, it sits within a wider Uniting Church structure involving property trusts, Synod governance, and the large operating platform of Uniting (NSW.ACT).

Public financial statements from that wider system report revenues in excess of a billion dollars and a substantial property base. Those figures are verified, but they describe the broader church-services ecosystem, not UTC itself.

The defensible conclusion is not that UTC is financially strong or weak on the basis of those accounts, but that it is not a transparent, standalone college balance sheet.

It is a ministry campus embedded within a much larger institutional system, where property, services, and governance structures combine to sustain its operation.

That gives it resilience in one sense.

And opacity in another.

6. The Real Divide

When you step back, the fault line becomes clear.

The divide is not primarily theological or denominational. It is economic.

Some institutions are sustained by time: assets, reserves, and foundations that allow them to absorb pressure. Others are sustained by flow: enrolments, fees, and partnerships that must hold year by year.

Both can function.

But they behave very differently when conditions tighten.

Stewardship

This point in the analysis is where the question sharpens for me.

When I consider the total assets invested in theological education and the number of leaders produced for churches and ministries, I find myself asking whether we are stewarding this well.

There are examples of wise, disciplined leadership. And some examples concern me.

I struggle with models that convert long-term assets into short-term cash to sustain ongoing deficits without a credible pathway forward. That is not innovation. It is the erosion of capital, of optionality, and ultimately of the very distinctives those assets were meant to protect.

And I find the assumption that denominational distinctives must always require separate institutional structures harder to sustain when the financial cost is this high.

Conclusion

What are we expecting to change to reverse this trajectory: more students, more funding, or a renewed pipeline into ministry?

I am praying and working for greater mission effectiveness across our nation. But if the numbers continue to decline, the question becomes unavoidable:

What is the long-term future of our current model of theological education?

In the next article, we will explore the responses emerging across the sector. Not simply innovation, but which adaptations actually strengthen resilience—and which simply defer the underlying pressure.

Because once you see the balance sheet clearly, adaptation is no longer neutral. The capital beneath it shapes it.

Geoff Folland

National Director

Power to Change